Embracing AI — why it’s time and how to get there

Future-proofing your lending business has to be a multi-pronged approach

Why do chefs say a knife is their favorite utensil? Because a spoon and a fork just don’t cut it. Ba-dum-bum-tss.

Do you feel like your current lending practices aren’t cutting through the noise of uncertain economic shifts and the competition from other lenders and fintechs? Has your confidence dulled because of market instability? Have you deployed new technologies just to find them falling flat?

Maybe it’s because you need a multi-pronged — or forked — approach to finding technology that uplevels your lending practices. Cutlery jokes aside, this is the exact approach I’d suggest credit unions take to their lending business.

Solving against the tough road that lies ahead won’t happen by cutting straight through your obstacles — credit unions need a technology partner with a multi-pronged strategy for recession-proof lending. This happens when you shore up your confidence on who you’re lending to, improve efficiencies in your business, and enable better lending decisions in general. AI credit decisioning can help you do it all, and Zest AI is the partner that is there every step of the way.

Why be in the knowhow on AI-based lending?

Not to say everyone is thinking about AI — but many folks are.

When it comes to investments in, use of, and creation of AI-banking products, J.P. Morgan Chase, Capital One, and Wells Fargo are in the lead. Large credit unions are using technology to advance their place in the industry, but they can afford to try out the shiny new toys in the market.

While commitment to innovation always gets a thumbs up from me, we know smaller credit unions might not have the capital — and sometimes subject matter experts — needed to invest in top-in-class innovation and find the right, long-term AI technology partners. How do you sort through the glitz and glamor that some technology providers will offer you when it comes to AI underwriting? Will a complex algorithm make loan underwriting lead to smart lending decisions? Does your small credit union actually need AI, and how would you even afford it?

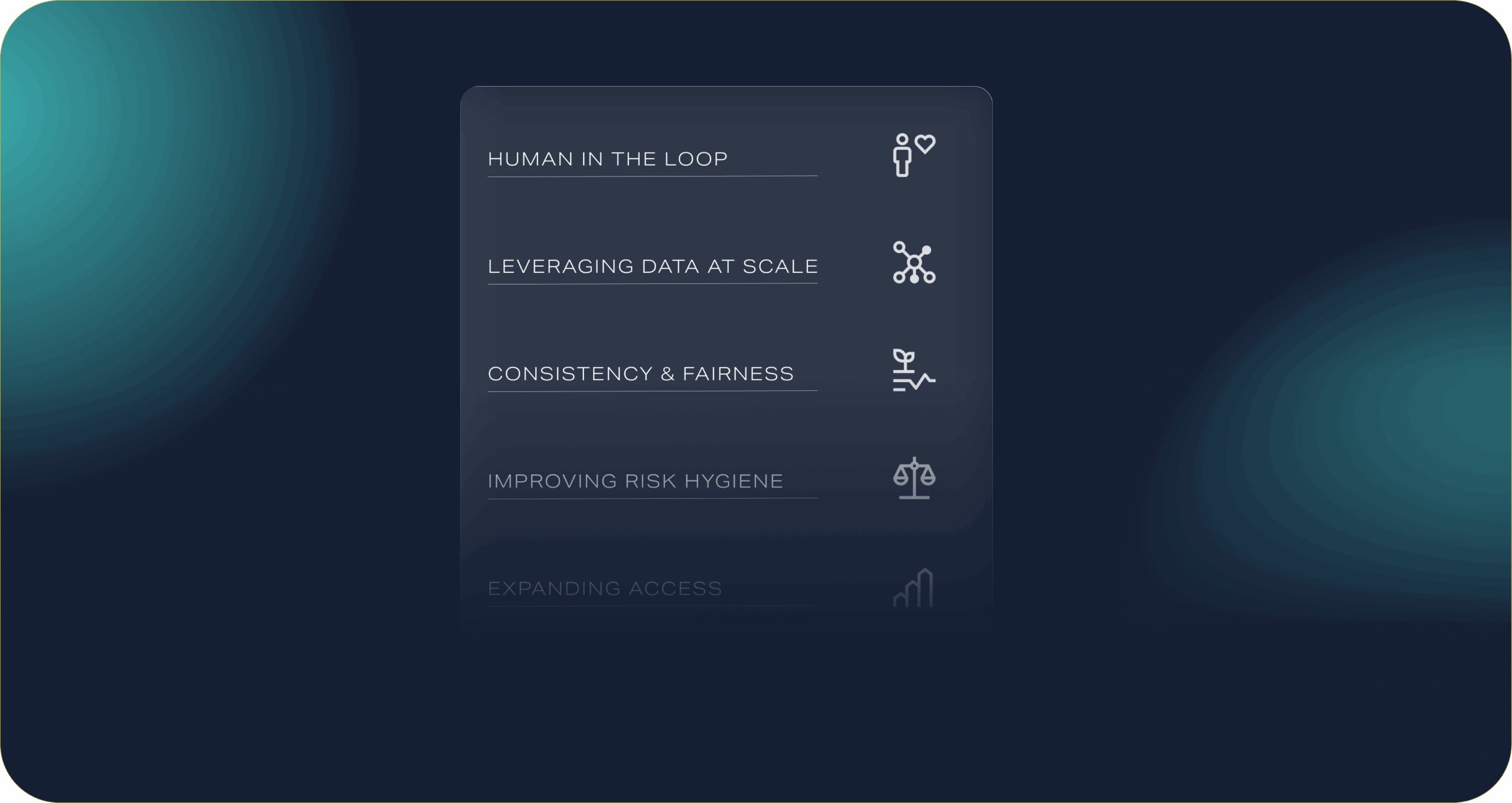

AI is essential for every size of credit union. Here’s some benefits our clients see because they’re using AI for their consumer loans.

- AI risk management – transparency into member data insights boosts confidence in compliance

- Better underwriting experience – AI optimizes your lending business, aiding credit unions to meet their members’ technology expectations

- More accessible lending – more accurate lending down the credit spectrum helps a greater percentage of a credit union’s community and produces a greater yield

I’ve said it before, but to reiterate, we’re here for you — big or small, good economy or bad, inflation, recessions, market shifts, unexpected changes, all of it.

How to evaluate AI-automated lending technology at every level

It’s time for all credit unions to incorporate AI into their core business operations. AI is a game changer and can realistically connect in and enhance all the strategic prongs your business has ahead of it. From beginning research to using the tech, exactly how your technology partner will plug into every part of your business strategy should be clear.

We begin by beginning

So you’re at the start of your AI journey? No problem!

A Fannie Mae survey from 2018 found that nearly 1 in 5 credit union executives said among the biggest reasons they had not adopted machine learning was that they didn’t know where to start. We spoke to some banking leaders at Money 2020 back in 2021, and 24 percent of respondents described their current underwriting technology as outdated… but 83 percent said AI would lead to better credit scoring. There’s a lot of confusion still out there about what AI is and how to use it. Education is key at this step of the process, and while I’ll promote personal research, we delved deep into AI and machine learning in a recent ebook.

Talking to technology partners about AI

This is the pivotal step in the process. Your decision will determine the ease of implementation of your chosen technology, the results you can achieve as a business, and how your business actually fares across different economic outlooks.

Success here looks like a technology partner who’s answering all of your questions, giving you insights into how this technology will work for your business, and showing you all the ropes regarding deployment and using this technology every day.

Deploying your new AI technology

Sometimes we don’t know the questions we need to ask until we’re in the moment of a question. This is why your technology partner can’t just hand you some technology once the contract is closed and peace out. AI can be complex, so when you’re a smaller credit union, or you don’t employ data scientists, and these unasked questions come up — you need someone to call.

Find the AI partner who will be there for the entire journey, who makes the implementation simple with low-lift IT measures for your lending teams, and who is just a call away.

Keeping your AI practices up-to-date

Finding compliant, explainable AI is at the top of every lenders’ to-do list — so when you find an AI technology partner who’ at the top of their game when it comes to compliance, it’s a lot easier to trust that your lending decisions are pristine. And when you can trust your AI underwriting to be smart, efficient, and accessible to all, you can reallocate resources previously spent on loan decisions to other parts of your business.

The AI technology you use matters at every level of engagement. Don’t let AI be a fork in the road — make it a new prong to future-proofing your organization, helping you run more efficiently, resource better, and reduce friction.

_____________________

Aaron Long — Head of Business Development

Aaron is a native of St. Louis MO and currently resides in Atlanta, GA with his two teenagers. He believes people are the core of every business and if you invest in them, you are investing in the long-term success of your company. Aaron has spent over twenty years leading teams that are motivated to win together and partnering with clients to ensure their success.