Decoding First-Party Fraud: When your best customers become your biggest risk

Is your customer who they claim to be? The growing threat of first-party fraud

Some lending losses don’t set off alarms immediately. An application looks clean. Identity checks out. Credit appears stable. The account opens smoothly, payments arrive on time, and the borrower may even qualify for a line increase. For months, everything tracks exactly as expected.

Then something shifts. Utilization climbs. Payments come later, until they stop altogether. Outreach goes unanswered. What once looked like a rock-solid borrower unravels, revealing something far harder to detect: first-party malicious intent.

Here’s the kicker: the borrower is real, and the data may be accurate, yet repayment was never part of the plan. Because identity checks out and early performance looks healthy, these accounts often get absorbed into traditional credit risk models. But the underlying driver isn’t hardship—it’s intentional behavior. Recognizing that difference changes how lenders measure losses and design protective safeguards.

A different kind of risk

First-party malicious intent lies between two familiar categories. In third-party fraud, identities are stolen or synthetic and the consumer is a victim. In traditional credit risk, borrowers intend to repay, but life events such as job loss or medical bills can make repayment difficult.

Intent risk is trickier to spot. Fraud teams see successful verification and credit teams see stable payment behavior. Because the account has demonstrated acceptable performance, exposure is often much higher when risk finally becomes visible. Credit lines may have increased and balances may have grown. That combination of legitimacy and delayed deterioration creates blind spots across fraud detection and credit monitoring.

Why losses can add up quickly

These cases may represent a small share of accounts, but their impact is outsized. Borrowers who maintain good standing early on, often build larger balances before default. When utilization is high at the point of default, loss severity rises sharply and charge-offs increase.

The ripple effects extend across the organization. When intentional defaults blend into general credit losses, portfolio signals get distorted. What looks like credit deterioration may actually mask coordinated, intentional behavior. This misreading leads lenders to tighten underwriting across entire segments, reducing approvals for strong applicants while the actual loss drivers remain unaddressed. Pricing and policy decisions are built on faulty assumptions.

Operationally, these accounts create a real drag. Collections teams chase cases with minimal recovery potential, disputes pile up, and reputational risk grows as patterns attract regulatory scrutiny. Strategically, the risk compounds when growth channels or new products become targets for exploitation, forcing lenders to pump the brakes on expansion or abandon promising segments. So, how can lenders spot warning signs and minimize first-party fraud risk?

First-party fraud banking types that drive portfolio damage

Malicious intent typically falls into one of four distinct patterns:

- Bust-out behavior: A borrower establishes a solid payment record, builds credibility, then rapidly increases utilization before ceasing payments.

- Sleeper accounts: Accounts perform normally for months, sometimes long enough to trigger a line increase, before deteriorating quickly and breaking all contact.

- Identity-controlled first-party misuse: An individual uses their own identity to obtain funds with no intention to repay.

- Collateral or asset extraction: A loan is used to pull out cash or liquidate an asset, with the borrower walking away soon after.

What connects these scenarios is the pattern itself. Early signals may appear ordinary, such as seasonal spending shifts, modest changes in payment timing, or a request for a higher limit. Risk becomes clearer as behaviors cluster, accelerate, and evolve together.

Why application fraud detection is challenging

These cases are hard to detect because they look legitimate at first, the identity is real, documentation checks out, early account behavior actually reinforces trust, and warning signs are typically subtle. A spike in utilization or a small shift in payment timing rarely justifies action on its own.

Effective application fraud detection requires connecting weak signals and tracking behavioral changes over time. The catch is that tactics are constantly evolving. As lenders close gaps, bad actors adjust and test new angles, so detection strategies need to evolve just as quickly.

What a smarter response looks like

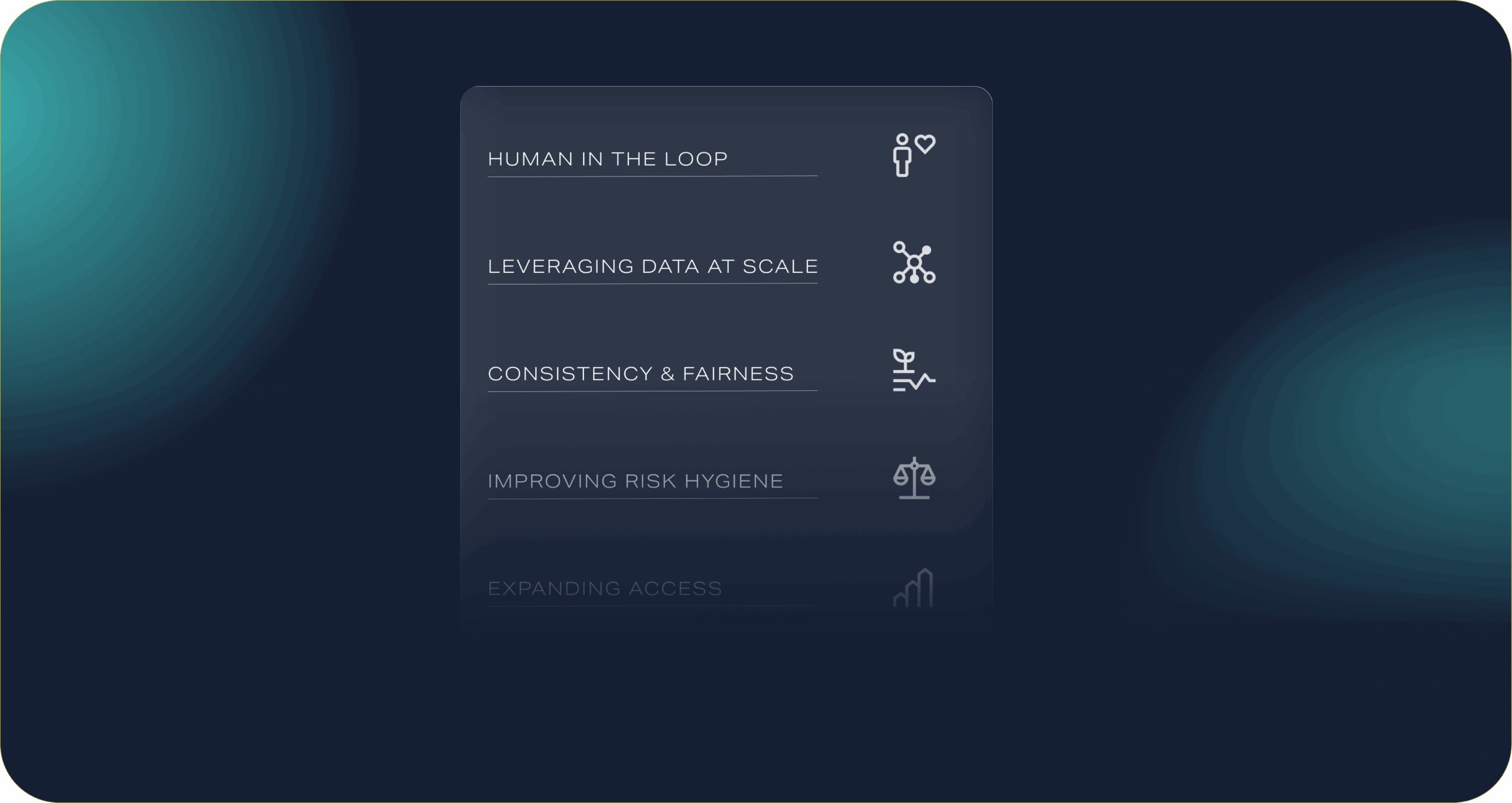

Addressing first-party malicious intent works best when you treat it as an intent issue, not solely a credit issue. Bringing credit and fraud perspectives together allows for sharper, more precise decisions. Here’s what that looks like in practice:

- Focus on early signals: Monitor unusual application patterns, identity or device anomalies, income or tenure inconsistencies, rising balances, shifts in payment or line-seeking behavior, and changes in responsiveness.

- Apply friction selectively: Introduce stepped-up verification, staged exposure, or moderated line increases only when multiple risk indicators appear, avoiding broad tightening that penalizes your good borrowers.

- Layer detection tools: Combine advanced models to uncover subtle behavioral patterns, structured rules to enhance transparency and explainability, and human review to manage edge cases.

- Share and seek out knowledge: Participate in information-sharing networks to stay current on emerging behaviors and strengthen detection capabilities.

Together, these approaches can help protect your portfolio while preserving a fair experience for most borrowers.

Measuring progress

Clear metrics turn strategy into measurable outcomes. Lenders often track early default rates, utilization at default, and the share of accounts that perform well before a sudden decline. Comparing approval rates alongside loss trends helps teams balance growth and risk. Pilots and back-testing allow organizations to refine thresholds before rollout, improving segmentation and pricing accuracy.

Protecting growth without pulling back too far

By combining lifecycle analytics, cross-functional collaboration, and adaptive modeling, lenders can identify intent risk earlier and respond with greater precision. The result is stronger performance, steadier approval rates, and sustainable growth.

At Zest AI, we help lenders use explainable machine learning to uncover behavioral patterns, including first-party bank fraud and intentional default. Our models surface risk earlier, so you can intervene sooner and cut avoidable charge-offs. As fraud evolves, your defenses need to keep pace. Contact us today and put smarter detection to work for your organization.

People also ask:

What defines first-party fraud?

First-party fraud is defined by intent. The borrower’s identity and application details may be legitimate, and early payment behavior may appear normal. What distinguishes it is the deliberate plan to take credit, cash, or assets without repaying.

What is second-party fraud in banking?

Second-party fraud typically involves a real customer knowingly letting another person use their identity or account to commit fraud. Unlike third-party fraud, the account holder is complicit, rather than a victim.

What is an example of first-party fraud in banking?

A borrower opens a credit card using their real identity, makes on-time payments for several months, and earns a line increase. After building a $15,000 balance, they suddenly max out the card and stop paying. The account looked healthy, but repayment was never the plan.

What is the difference between first and third-party fraud?

First-party bank fraud involves a real customer using their own identity to obtain credit or funds with no intention of repaying. Third-party fraud occurs when a criminal uses a stolen identity, turning the real consumer into a victim.

Is first-party fraud illegal?

Yes. Even though the borrower’s identity is real, intentionally taking credit or funds without planning to repay is considered fraud.

What are red flags for first-party fraud?

Warning signs often appear in patterns rather than single events. These may include sudden increases in utilization after a period of steady performance, requests for line increases followed by rapid balance growth, subtle shifts in payment timing, or reduced responsiveness to outreach.